What is a personal balance sheet?

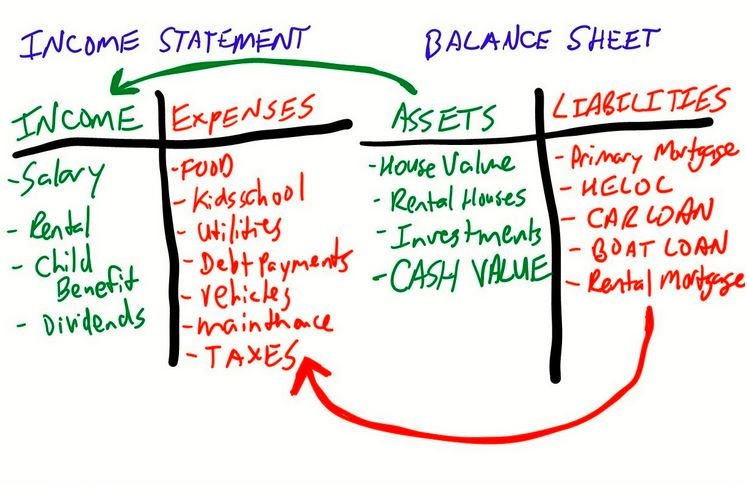

A personal balance sheet Also referred to as a personal financial statement, a personal balance sheet is a document that outlines an individual’s personal financial position at a given time, detailing the liabilities, assets.

Do you know your net worth? Find out your worth by creating a personal balance sheet. It helps you find out if you are on the right path to achieving your goals. A personal balance sheet will highlight your asset values and the total of all debts you have. The result is how much you are worth.

Unlike an expenses spreadsheet or a budget, a financial statement gives you a bigger picture than your day-to-day spending habits. While it may take you some time to create a personal balance sheet, it is totally worth it. It shows the difference between assets and liabilities- if your assets are more, then it means you can sell your assets to pay off your debts. If the liabilities are more, then you have a negative net worth. Additionally, knowing your financial position allows you to avoid unnecessary declined credit applications. It is also helpful to see where the concentration of your net worth sits. If you have all of your net worth tied up in your principal residence equity and have no other assets will that support your long-term goals?

What Should I Include in My Balance Sheet?

Of course, you can have investments and savings that exist outside of these official account types. Most would consider their stock or open mutual fund portfolio or cryptocurrency accounts and even income properties themselves as retirement account. They are investments, yes indeed, but not explicitly classified as retirement accounts.

Start by filling in your basic information, such as your name, job description, and contact details. Just as the description suggests, you should then list your assets and liabilities. Think of every income and investment stream, such as real estate investments, annual salaries, and retirement plans. Possible assets include:

- Bank accounts balances

- Guaranteed Interest Certificates (GICs), bonds and treasury bills

- Valuables such as jewelry

- Gold, silver, bullion or other precious metal assets

- Real estate investments, what are they worth if you sold them today

- Investment accounts such as RRSPs, TFSAs, RESPs, RDSPs, LIRAs, any company or union pensions, mutual fund, segregated funds, stocks and even the very popular cryptocurrency accounts

- receivables from your business (people who owe you money)

- Loan assets, where you have lent money to someone, such as a second mortgage on a property, where you are the bank, not the borrower. This could even include a shareholder loan to your corporation or a business you own that needs to pay your back.

- And the least known asset that is often the most powerful on your balance sheet is cash value from life insurance policies.

Additionally, if you are trying to appease the bank for financing purposes, you may add up some other depreciating personal items. In the real financial world, no one truly considers these assets…but your bank wants to know everything they could possibly take collateral on. Therefore you can also total up these type of items:

- Car’s and trucks

- motorcycles

- RV’s, camping trailers

- Recreation vehicles like boats, snowmobiles, quads, etc

Liabilities, on the other hand, diminish your net worth. They will show up in another column and get subtracted from the total of all your assets. They may include:

- Outstanding loans

- Mortgages and Home Equity Lines (HELOC)

- Credit card balances and personal credit lines

- Outstanding federal, provincial taxes or property taxes

- Personal debts, such as a loan from a parent

- Bank overdraft accounts

Today, there is a current need for individuals to determine their worth. However, most Canadians do not realize that Par Whole Life Insurance Cash Value should be listed as their assets. It is basically just like home equity. Par Whole Life Insurance Cash Value could be your best-performing asset. What’s more, it could supplement or, better yet, replace your retirement income. Continue your journey of learning and discover more about this powerful asset class.

Check out our videos, podcasts, and articles to get a deeper insight into why Par Whole Life Insurance Cash value is one of your best assets.

New Training from Jayson Lowe:

Infinite Banking Concept

At Ascendant Financial we have expert financial advisors and coaches that can help you understand all your options with Personal Balance Sheets. Register for our training so that you can book a time with your own advisor

Popular Posts

- Whole Life vs. Universal Life Insurance: Which is Right for You?

Choosing the right life insurance policy can feel like one of the most important financial decisions you will make. With so many options, it can… Read more: Whole Life vs. Universal Life Insurance: Which is Right for You?

Choosing the right life insurance policy can feel like one of the most important financial decisions you will make. With so many options, it can… Read more: Whole Life vs. Universal Life Insurance: Which is Right for You? - The Comprehensive Guide to Life Insurance Retirement Plans (LIRPs)Planning for retirement is a critical step in securing your financial future, but it’s not just about saving money—it’s about making smart decisions to grow… Read more: The Comprehensive Guide to Life Insurance Retirement Plans (LIRPs)

Share This Post

Categories & Tags